[ad_1]

To maintain the operating gag going: No fish this time and only some ships, however loads of different stuff on this random choice of 15 Norwegian shares. 4 out of those 15 certified for my prelimiary “watch” listing. Let’s go:

91. Wilson ASA

Wilson is a 270 mn EUR market cap shiping firm that operates ~130 smaller vessels. As different delivery firms, they trades at very low valuations, on this case 3,5x 2022 P/E. Working margins have elevated from 2,5% to 40% in 2022. I don’t know how sustainable these margins are, however traditionally the height has been round 20% and on common possibly 10-15% with a excessive volatility. Apparently, the share worth hovered round 20 NOKs for 20 years earlier than going up greater than 3x in 2021:

However, unstable delivery shares will not be my space of experience, “cross”.

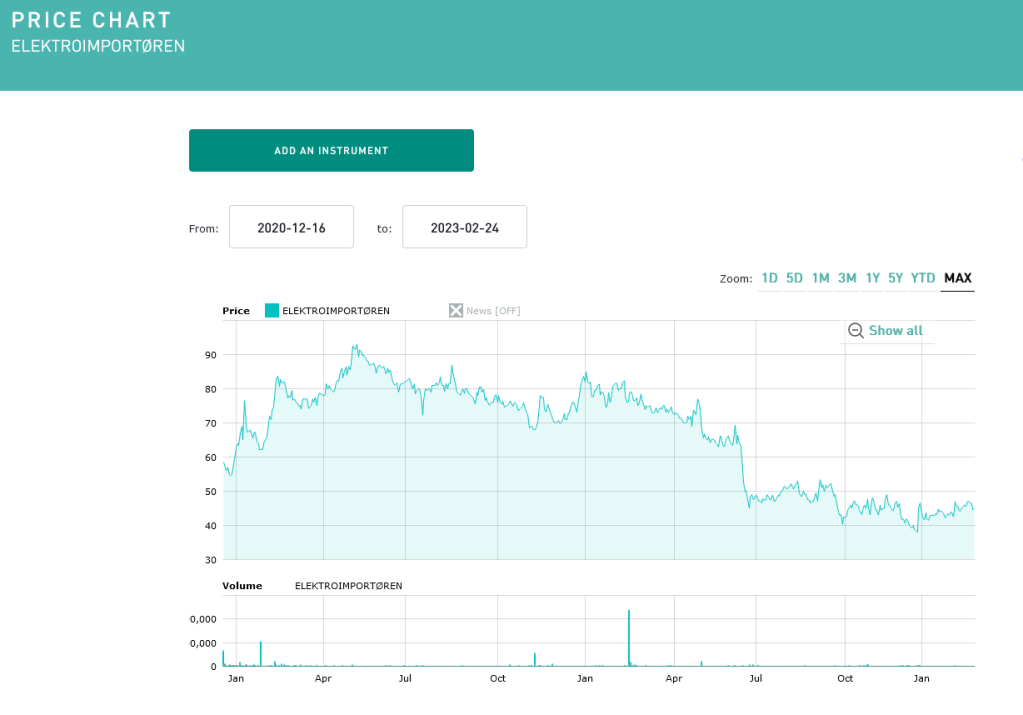

92. Elektroimportoeren ASA

Because the title indiactes, this 84 mn EUR market cap firm retails and distributes gear for electrical installations (gentle, electrical energy and so on.). The corporate has grown properly over the previous 5 years, nonetheless EPS halfed in 2022 which led to a big drop within the share worth under the extent of the IPO in 2020:

They appear to have entered the Swedish market in 2022 however total, Gross margins and like-for-like gross sales struggled and curiosity bills elevated, resulting in a giant discount in income. At 19x trailing p/E and 15x trailing EV/EBIT, the inventory isn’t low cost and the IPO appears to have been “properly timed”. “Cross”.

93. Entra

Entra is a 1,9 bn EUR market cap actual property firm that largely owns workplace buildings in Norway. The inventory misplaced virtually -50% from its high, much like many different actual property shares. I at all times discover it exhausting to grasp the industrial actual property KPIs like EPRA NAV and these things, their P&L is kind of messy because the present mark-to-market positive factors and losses within the P&L. Actual property is one thing I might solely take into account in very particular circumstances which this isn’t. “Cross”.

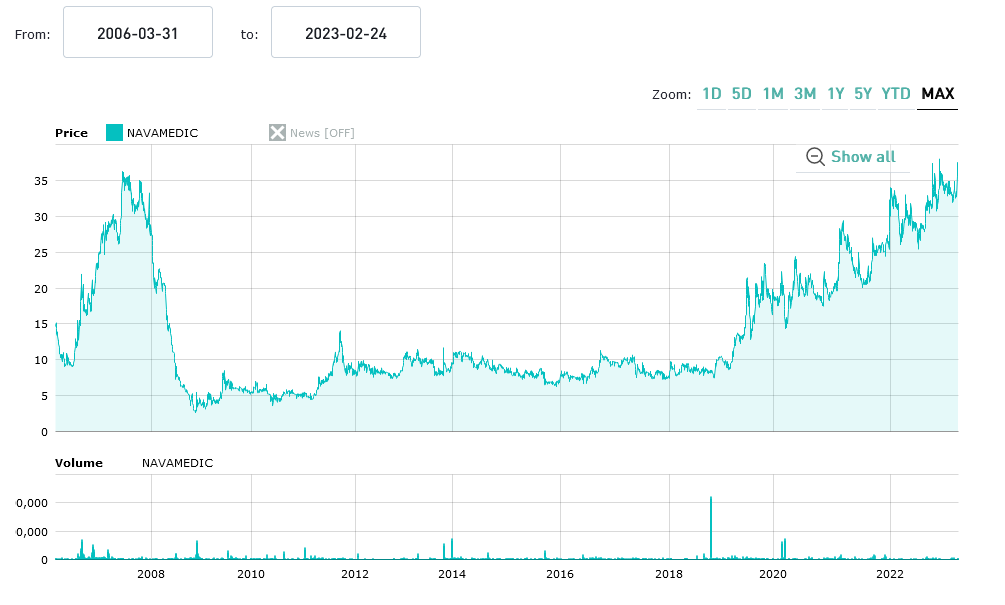

94. Navamedic

Navamedic is a 57 mn EUR market cap “Nordic pharma firm supplying hospitals and pharmacies with pharmaceutical and medical diet merchandise”. The corporate has been loss making for a few years however, surprisingly, turned worthwhile in 2022. That is mirrored within the share worth which is now near ATH:

The corporate appears to have a large protfolio of OTC and prescribed drugs in addition to “medical diet” with some deal with obesitiy, but in addition antibiotics and different stuff. At lower than 20x P/E, the inventory isn’t too costly and the corporate plans o develop through M&A and so on to 1bn NOK in income and 150 mn NOK in EBITDA. In the meanwhile, I’ll put them onto the prolonged “watch” listing

95. Cyviz

Cyviz is a 44 mn EUR market cap “international know-how supplier for standardized convention rooms, management rooms and expertise facilities.” The corporate was IPOed in December 2020 and is loss making, however based mostly on TIKR at the very least money circulate optimistic.

If I perceive their enterprise appropriately, they set up management rooms for the protection sector in addition to prime quality board rooms atc world wide:

One way or the other I discover this firm fairly fascinating, particularly as it’s nonetheless rising fairly rapidly (+50% full 12 months, +80% q-o-q). This appears to be one of many higher 2020/2021 IPOs, subsequently “watch”.

96. Elliptic Laborator

Elliptic is a 160 mn EUR market cap firm that does some “”attractive” issues like “AI Primarily based 3D gesture Software program sensors”. Nevertheless, Income is simply 5 mn EUR, stagnating and they’re making losses. One of many weaker 2020/202 IPOs, “Cross”.

97. ATEA

ATEA is a 1,2 bn EUR market cap “main Nordic and Baltic resolution supplier of IT infrastructure with over 7,000 staff. Atea is current in 85 cities in Norway, Sweden, Denmark, Finland, Lithuania, Latvia and Estonia. “

With working margins of 2-3%, the bsuiness mannequin appears to be extra of a reseller or distributor. The corporate is comparatively reasonably valued at 14x P/E and return on capital/fairness is at the moment at round 20% or extra.

Atea has internet money, is paying a relatively beneficiant dividend (~5% yield) and has been rising properly over thy previous few years. The share worth nonetheless doesn’t absolutely mirror this:

Though related IT distributors are equally low cost, I put ATEA on “watch”.

98. Inexperienced Minerals

Inexperienced Minerals is a 5 mn EUR Nano Cap that claims to be the ” pioneer in marine minerals on the Norwegian Continental Shelf”. The corporate has little income and is burning cash, with a runway of lower than 2 years left. “Cross”.

99. Norwegian Block Change

This 10 mn EUR market cap 2021 IPO runs a Crypto change. After all they’re burning money and so they have raised addtional cash in Q3 2022. “Cross”.

100. Questback Group

Questback is a “main platform for conducting Worker and Buyer Expertise surveys”. The market cap of solely 5 mn EUR signifies that enterprise isn’t so nice. They’ve been rising in 2022 however are CF detrimental and have substantial debt. Additional fairness financing is probably going required as they’ve lower than 1 12 months runway left. “Cross”.

101. Precise Therapeutics

Precise is a 31 mn EUR market cap inventory that IPOed in 2022 and misplaced round 2/3 of its worth since then. They develop know-how ” for focused therapeutic enhancement – Acoustic Cluster Remedy (ACT®). ACT® sonoporation is a novel strategy to ultrasound-mediated, focused drug enhancement”, no matter which means. The corporate has no revenues, “cross”.

102. Solstad Offshore

Solsatd is a 320 mn EUR market capo firm that “operates offshore service and building vessels for offshore and renewable vitality trade worldwide. It supplies platform provide vessel, anchor dealing with vessel, subsea building, and renewable vitality companies.”.

Wanting on the inventory chart, the corporate went by means of exhausting instances and was restructured in 2022 together with a debt-to-equity swap.

Operationally, issues look comparatively good as of late, however the firm nonetheless carries loads of debt (~2 bn EUR) and is making losses on GAAP foundation. Largest Shareholder appears to be Aker who snapped up different Norwegian gamers up to now. “Cross”.

103. Adevinta

Adevinta is a 8,4 bn EUR market cap on-line classifieds firm that was spun-off from Schibsted in 2019. Schibsted owns ~34,8% and apparently Ebay owns virtually the identical quantity. Wanting on the chart, we are able to see that originally the inventory perforemd very properly earlier than than affected by 2022 on:

The enterprise as such seems enticing. Excessive progress charges (+40% in 2022) and respectable working margins. Nevertheless, a big Goodwill impairment in 2022 led to a GAAP loss.

Primarily based on the projections, the inventory is valued a ~15x EV/EBITDA for 2023 and so they count on to develop at “low double digits” for the subsequent years. Though the inventory isn’t low cost, it’s defintely one to “watch”.

104. Nel ASA

Nel is a (a lot hyped) 2,2 bn EUR market cap firm that’s lively within the Hydrogen Financial system. Nal manufactures Electrolyzers and Hydrogen Filling station gear. Wanting on the chart we are able to see that Nel has been round for a while and had a frist hype cycle simply earlier than the monetary disaster:

In comparison with different firms in that house, NEL truly does have gross sales (~90 mn EUR in 2022), however isn’t making a living. Losses are literally increased than gross sales. Personally, I don’t consider in a mass marketplace for Hydrogen as a automobile or truck gas at the very least for the subsequent 10 years or so, therfore I’ll “cross”.

105. Arctizymes Techno

This “fancy title” firm has a market cap of 180 mn EUR does one thing with enzymes and shocking to me is definitely making a small revenue. However, at round 13xEV/Gross sales and 50x EV/EBIT with solely reasonable progress, I don’t suppose that that is fascinating. “Cross”.

[ad_2]

Source link