[ad_1]

International information protection has been paying a whole lot of consideration to the latest regulatory developments addressing scams in Europe and in the UK. However these usually are not the one locations the place vital rip-off regulation and protection enhancements are being deployed.

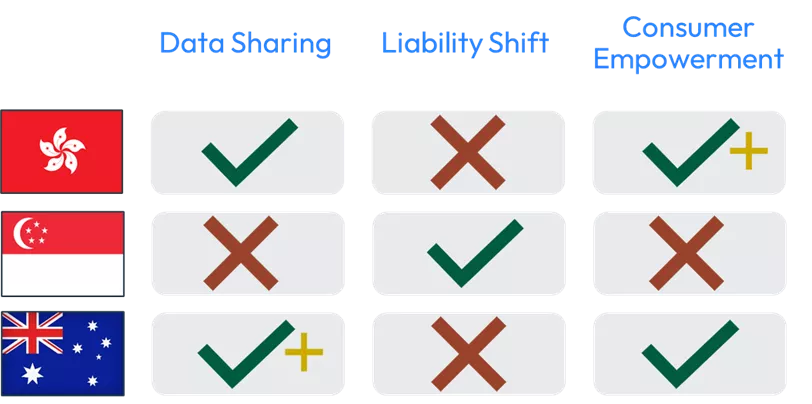

On this put up we delve into how three nations in Asia Pacific are taking their very own method to combatting scams. Particularly we’ll look at Hong Kong’s progressive fraud alert system that bolsters shopper confidence, Singapore’s Shared Accountability Framework which outlines duties and tasks of not solely the monetary establishments (FIs), but additionally telcos, and Australia’s complete Rip-off-Protected Accord which needs to take knowledge sharing to the subsequent degree.

In my view these various approaches to defending shoppers and preserving the integrity of their monetary programs will likely be an inspiration for regulators in different nations within the area and the world. These adjustments may even encourage fraud and threat leaders to marvel and debate what’s subsequent for them.

Empowering Hong Kong Customers with Rip-off Prevention Instruments

In Hong Kong, the rise of digital transactions has been paralleled by a rise in monetary scams. In response, Hong Kong has applied a pioneering fraud alert system, setting a brand new commonplace in shopper safety and rip-off prevention that goes past what many govenments and nations use in the present day within the type of Affirmation of Payee.

The initiative is a major collaborative effort, bringing collectively the Hong Kong Police Power, Hong Kong Financial Authority (HKMA), The Hong Kong Affiliation of Banks, and 44 main retail banks. The answer, built-in into the Sooner Cost System (FPS), permits for police and authorities officers to develop instruments that buyers can use to higher defend themselves from scams.

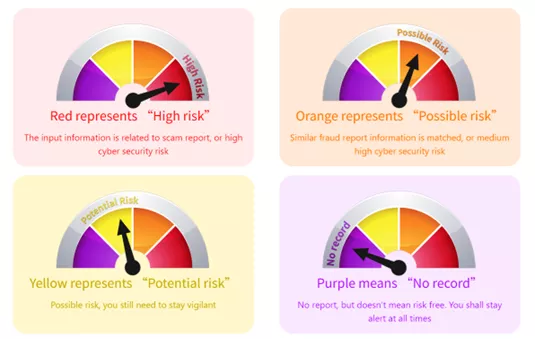

On the coronary heart of that is Scameter, a cellular app that notifies customers of high-risk transactions in actual time. When a recipient’s proxy ID (telephone quantity, e mail deal with or FPS identification code) on a FPS transaction is deemed as “Excessive Danger” within the Scameter, the consumer of the appliance receives a right away warning. This immediate alert mechanism empowers shoppers to make knowledgeable selections, serving to defend them in actual time and considerably decreasing the chance of falling prey to scams.

Within the picture under you possibly can see the kind of alerts the Scameter app would possibly present to the particular person initiating the cost (picture courtesy of Cyber Defender Hong Kong).

Regardless of these technological and knowledge sharing developments, Hong Kong’s regulatory our bodies stay vigilant, recognizing and highlighting to shoppers that the absence of an alert doesn’t assure transaction security. In contrast to some regulators throughout the globe, Hong Kong’s regulatory physique has not indicated any plans to alter the principles across the legal responsibility for the loss due to a rip-off, neither in favour of the patron nor by placing extra strain on the receiving establishment.

The options deployed by Hong Kong assist to empower the shoppers to have the ability to self-validate extra successfully whether or not the cost they’re making is a rip-off or not. However do they go far sufficient in coping with the issue and making certain the belief of buyer within the cost community? And can the shoppers proceed to be chargeable for loss even when the Scameter doesn’t point out a threat?

I think these usually are not the final measures Hong Kong will likely be implementing to mitigate scams.

Singapore’s Waterfall Shared Accountability Framework

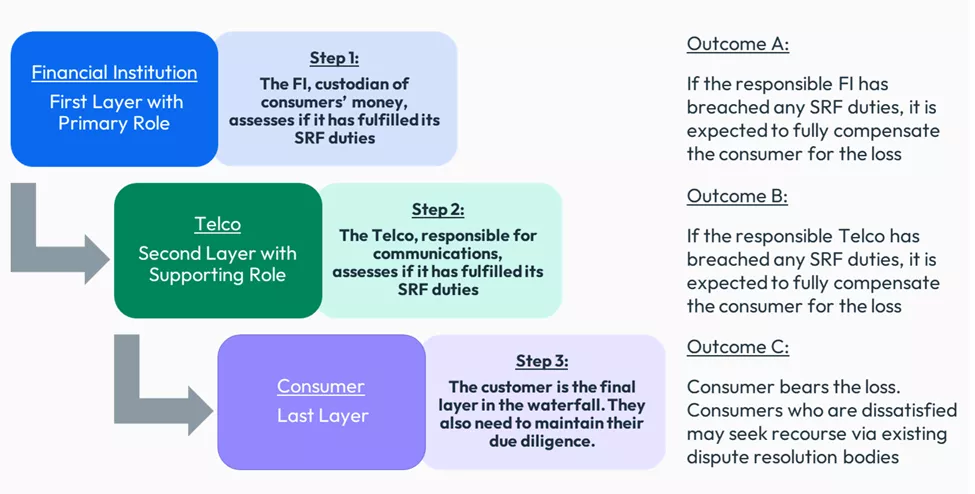

In Singapore’s dynamic digital financial system, the problem of combating monetary scams has led to the proposal for the Shared Accountability Framework (SRF). Led by the Financial Authority of Singapore (MAS) and Infocomm Media Growth Authority (IMDA), the SRF represents a groundbreaking shift in rip-off prevention. It advocates for a collective accountability mannequin, allocating rip-off loss tasks amongst monetary establishments (FIs), telecommunication operators (telcos), and shoppers. This method goals to foster a extra built-in and cooperative ecosystem for digital transaction security.

The SRF emphasizes the necessity for FIs and telcos to implement strong anti-scam measures. The framework considerably elevates the usual of shopper safety by making certain that the entities instantly concerned in cost ecosystems or communication channels utilized by the fraudsters are extra accountable for rip-off losses.

Below proposed legislative frameworks, these establishments must pay victims of scams if they’re discovered to have come up quick in fulfilling their protecting duties outlined within the SRF laws, reminiscent of:

For banks:Impose a 12-hour cooling off interval upon activation of digital safety token throughout which “high-risk” actions can’t be carried out.Present notification alert(s) on a real-time foundation for the activation of digital safety token and conduct of high-risk actions.Present outgoing transaction notification alert(s) on a real-time foundation.Present a (24/7) reporting channel and self-service function (“kill change”) to report and block unauthorized entry to their accounts.For telcos:Join solely to approved aggregators for supply of Sender ID SMS to make sure these SMS originate from bona fide senders registered with the SSIR.Block Sender ID SMS which aren’t from approved aggregators to forestall supply of messages originating from unauthorized SMS networks.Implement an anti-scam filter over all SMS to dam SMS with recognized phishing hyperlinks.

Beneath you possibly can see the instance from the proposed laws, outlining how the waterfall method would work in apply:

Whereas these particulars are nonetheless going via a consultative interval earlier than the brand new regulation is formally in place, this provides us an excellent glimpse into what to anticipate from the Financial Authority of Singapore.

My expectation is that these measures will develop past simply monetary establishments and telcos and can incorporate social media suppliers sooner or later (the place most scams across the globe originate), and I’d not be shocked to see the checklist of duties anticipated of all individuals to develop.

The large query shopper safety teams will likely be asking is whether or not the legal responsibility change measure goes far sufficient in defending the unsuspecting victims, particularly in a world the place AI makes it tougher and tougher to inform actual from pretend.

Australia’s Complete Anti-Rip-off Initiative

Australia has additionally taken large strides in regulatory adjustments and launched the Rip-off-Protected Accord, a concerted initiative led by the Australian Banking Affiliation (ABA) and the Buyer Owned Banking Affiliation (COBA). This Accord exhibits dedication from Australia’s monetary establishments, together with community-owned banks, constructing societies, credit score unions, and business banks, to raise the usual of buyer safety and successfully counter scams. It is a response to the alarming statistic that Australians misplaced $3.1 billion to scams in 2022, marking an 80% enhance from the earlier 12 months. The Accord encompasses a sequence of complete anti-scam measures, aiming to disrupt, detect, and reply to the evolving rip-off threats.

Client safety teams have been lobbying the Australian regulator to observe among the different nations and deploy a Affirmation of Payee system. We will see the Australian regulator committing to that as a part of their technique with a $100 million funding in an industry-wide affirmation of payee initiative.

Different measures embody the necessities for biometric checks for brand new on-line accounts, enhanced warnings, and delays for brand new payees or elevated cost limits, and most significantly for the complete affiliation to return collectively and put money into an expansive intelligence-sharing community throughout the banking sector. The target of this data-sharing initiative is to assist banks forestall extra scams and recuperate funds for patrons quicker and extra successfully.

Primarily based on earlier communication from the Australia’s Nationwide Anti-Rip-off Centre, I count on these measures is not going to cease on the monetary establishment solely, and the data-sharing mechanisms will develop past simply the banks. The regulators are already excited about increasing the info distribution to different industries, reminiscent of telcos, enabling them to dam a name, or digital platforms, which may take down an internet site or an account the place the rip-off has originated.

The large query that continues to be unanswered for now could be across the legal responsibility shift. Will the Australian regulator observe swimsuit with the UK and implement legal responsibility sharing between the receiving and originating financial institution? Will it take an analogous stance to Singapore with a waterfall method between totally different industries? Or will it depart the onus on the shoppers to remain vigilant and look out for themselves?

Rip-off Laws in Latin America

It’s intriguing to see how the subject of rip-off regulation is addressed throughout totally different nations, and taking a fast look at Latin America, one other area with paced quick development in real-time cost companies and digitally savvy shopper base, we see some similarities.

Brazil seems to be spearheading the regulatory adjustments within the area, with the latest deployment of Decision 6, a change that requires monetary establishments, cost establishments and different establishments approved to function by the Central Financial institution of Brazil to gather knowledge on fraudulent transactions and to share that knowledge.

They’re what is going on in United Kingdom, Europe & USA and are taking their very own steps to safe their very own cost ecosystem to take care of shopper belief within the extremely common real-time cost service Pix.

We count on to see developments and extra information popping out from Mexico, Colombia, and Peru. My colleague Pierre Isensee takes a deeper have a look at the present state of scams and regulation throughout the Latin America in his newest put up.

Put together for Scams Laws

The progressive and collaborative approaches to rip-off regulation in Hong Kong, Singapore and Australia provide priceless classes and insights into totally different options to combating monetary fraud. They every may have their professionals and cons, and I’m fascinated by how numerous and totally different the stances are taken by the regulator in every nation.

The main focus of their approaches is tailor-made in direction of minimal disruption to the cost ecosystem and instilling shopper confidence in real-time funds.

Nations throughout Asia are prone to observe and study from these options — adapting and implementing comparable methods tailor-made to their distinctive monetary ecosystems and shopper base.

What are the important thing areas that may see probably the most vital change over the approaching years?

1. Information Sharing & Collaboration

As regulatory approaches that incorporate knowledge sharing come into apply throughout many nations, I count on extra motion to develop data-sharing platforms & fraud investigative processes that goal for simplicity, pace and accuracy. On prime of that, we’ll see better emphasis on cross-border cooperation to additional investigations and coverage improvement, such because the Multilateral Memorandum of Understanding in Americas.

2. Client Safety

The pattern in direction of extra consumer-centric laws will proceed. We’ll see extra demand for legal guidelines that not solely forestall scams but additionally present strong assist and safety for victims (together with reimbursement). This shift will finally result in laws that put extra strain not solely on monetary establishments and telecom companies, but additionally on web service suppliers and social media networks to collaborate and make investments extra in rip-off preventative measures.

3. Client Empowerment

The main focus will stay to allow extra direct involvement of shoppers in rip-off prevention efforts, each via mass-marketing instructional campaigns and instruments that empower people to safeguard their very own monetary safety (reminiscent of Scameter or Australia’s just lately introduced Affirmation of Payee mission). On prime of that, I absolutely count on extra motion on this area in each the telco and social media industries, as they be part of efforts in highlighting dangerous accounts, telephone numbers and different flags that assist alerts recipients of potential scams.

4. Technological Developments

We’ll witness an elevated concentrate on the position of know-how not simply as a instrument for fraud detection but additionally as a method of fostering safer digital transaction environments. Developments in AI and machine studying will play vital roles in future regulatory frameworks, enhancing rip-off detection and decreasing shopper friction. We’ve seen the tempo at which AI has been shifting over the previous 12 months — we have to guarantee our instruments are maintaining with the know-how and usually are not left behind.

For instance:

Are my fraud instruments versatile sufficient to ingest any type of new info quickly and put it to use in my transactional decisioning in real-time?Do I’ve the means to simply customise & develop my buyer communication based mostly on a plethora of things and variables, construct intelligence into the messaging, and adapt it to new circumstances at a minute’s discover?Do I’ve the best instruments to make use of the good fashions my crew is constructing in-house, or do I get hampered by inefficiencies and technological restrictions that forestall me from deploying these fashions into manufacturing?Do my fraud prevention instruments permit me to guage knowledge and selections taken via the shopper lifecycle, from software via youth all the best way to prolonged life to make higher and extra knowledgeable selections?

For those who’re already dealing with such technological issues in the present day, they are going to solely develop and get compounded the extra superior AI and different know-how will get.

Primarily based on what we’ve seen across the globe, these monetary establishments which are considering forward within the regulation sport and serving to to drive the conversations with regulators are most poised for achievement when change does happen.

FICO’s fraud consulting crew stands prepared to assist clients in APAC deal with the problems raised by scams and new laws.

How FICO Helps Detect and Stop Scams

[ad_2]

Source link